Money laundering is a serious crime, and it can have devastating effects on both businesses and society as a whole. As such, it’s important for financial institutions and Fintech companies to have solid anti-money laundering (AML) best practices in place. In this blog, we’ll provide an overview of the AML best practices that every organization should be following.

Risk Assessments

The first step towards creating a comprehensive AML program is to conduct a risk assessment. This assessment will analyze the various risks associated with money laundering activities, such as customer identity verification, suspicious activity monitoring, and reporting.

By understanding the potential threats posed by money laundering activities, organizations can better prepare themselves to detect and prevent them from occurring.

Know Your Customers

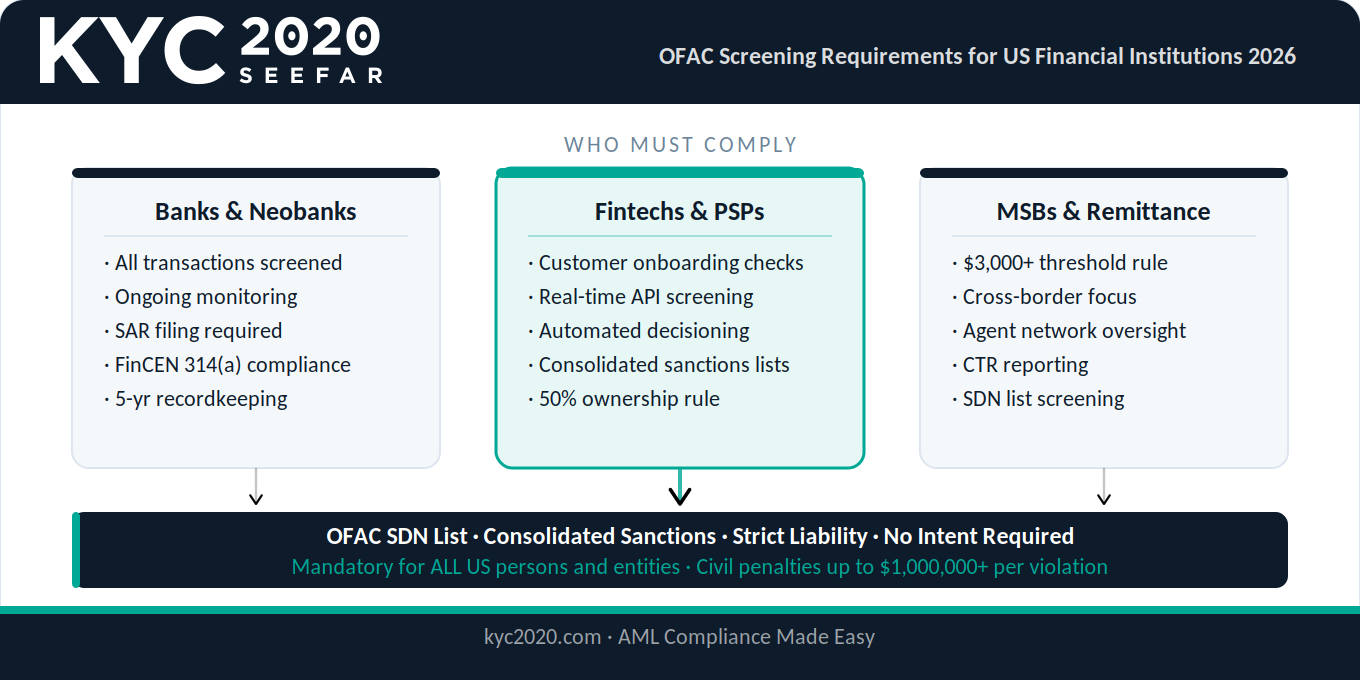

Any organization that deals in financial transactions should understand their customers’ backgrounds and profiles. This includes knowing who they are, where they come from, what type of business they’re involved in, etc. Knowing this information helps organizations better identify any suspicious activity that may be taking place within their network.

Additionally, organizations should also take steps to ensure that customers are not using false or stolen identities when conducting transactions.

Customer Due Diligence

Organizations must also perform regular customer due diligence checks to ensure that the people they are doing business with are not engaged in any nefarious activities or connected to any criminal organizations or individuals. This includes checking for any public records or sanctions lists that could indicate a customer might pose a risk to the company’s operations.

Organizations should also monitor their customers’ behavior over time to look out for any sudden changes in their financial activities which could signal illegal activity is taking place. Finally, organizations should make sure they have clear policies and procedures in place for dealing with potential violations of AML regulations by customers or employees.

5 Pillars of AML Compliance

1 – Risk Assessment

Risk assessment is a fundamental pillar of AML compliance. It involves identifying, assessing, monitoring, and managing the various risks associated with money laundering and terrorist financing activities. Companies should have robust risk assessment processes in place to identify potential risks.

Once these risks are identified, companies can then develop strategies for mitigating those risks. This should include policies and procedures for monitoring customer activity as well as implementing measures to prevent any suspicious activity from taking place.

2 – Customer Due Diligence

The second pillar of AML compliance is customer due diligence (CDD). This involves verifying the identity of customers who may be involved in money laundering or terrorist financing activities. Companies must collect sufficient information about their customers so that they can identify them accurately and detect any suspicious behavior.

This includes collecting information such as name, address, date of birth, nationality, occupation, source of funds, etc. It is important for companies to ensure that their CDD processes are up-to-date and compliant with all applicable regulations.

3 – Transaction Monitoring

The third pillar of AML compliance is transaction monitoring. This involves continuously monitoring customer transactions to identify any suspicious activity or transactions that may be related to money laundering or terrorist financing activities.

Companies should have systems in place to monitor customer transactions on a regular basis and alert them if any suspicious activity is detected. This includes monitoring customer accounts for unusual patterns or discrepancies in transactions, as well as reviewing customer profiles periodically to ensure accuracy and completeness.

4 – Reporting & Record Keeping

The fourth pillar of AML compliance is reporting & record keeping. Companies must keep accurate records of all financial transactions related to their customers in order to comply with applicable regulations. They must also report any suspicious activity or transactions that may be related to money laundering or terrorist financing activities promptly to the relevant authorities.

Keeping accurate records helps companies stay compliant by ensuring they have evidence available if required by regulators or law enforcement agencies during investigations into money laundering activities.

5 – Training & Education

The fifth pillar of AML compliance is training & education. Companies should provide their employees with adequate training on anti-money laundering legislation and regulations so they can identify signs of potential money laundering or terrorist financing activities quickly and effectively.

Employees should also be educated on how best to respond when such activities are suspected so they can take appropriate action promptly without compromising the integrity of the company’s operations or data security protocols.

Conclusion:

Adhering to anti-money laundering best practices is essential for any organization looking to protect itself from the risks posed by money laundering activities. By conducting risk assessments, knowing your customers’ backgrounds thoroughly, and performing regular customer due diligence checks, organizations can create effective AML programs that help keep them safe from these types of crimes.

Implementing these best practices can not only help your organization stay compliant with regulations but also safeguard its reputation as well as its assets from possible damage caused by money launderers operating within its network.