As technology becomes an ever larger part of our lives, the way we handle money is changing. For years now, FinTechs have been at the frontlines of this changing landscape, by providing customers with better, faster and more inclusive financial services. However this is not an isolated incident. Across every sector, agile, small and midsize companies (aka SMEs) are disrupting their industries by providing new, energizing customer experiences. It’s no great mystery why SMEs have become such a massive slice of the economic pie. The fact is, with the number of SMEs growing, the regulatory scrutiny and liabilities do so too. Now, more than ever, SMEs need to make sure they are meeting Anti-Money Laundering (AML) compliance standards or they risk massive fines.

Historically, SMEs have been at a disadvantage when it comes to Anti Money Laundering (AML) compliance solutions. Often times SMEs don’t have the infrastructure to do effective sanction screening. And for the companies that can accommodate the traditional process, it still may move too slowly for it to be truly efficient for their purposes. After all, when you sign up for a service online the expectation is to move through the process as quickly as possible. SMEs, particularly emerging payment innovators, need an AML compliance process that can match the speed of their businesses. As new markets emerge these emerging payment innovators grow more influential and thus come under greater scrutiny from regulatory bodies. As that pressure mounts, SMEs must strengthen their AML compliance regimes. They need the right tools for the job.

Why not Just use the Existing Tools?

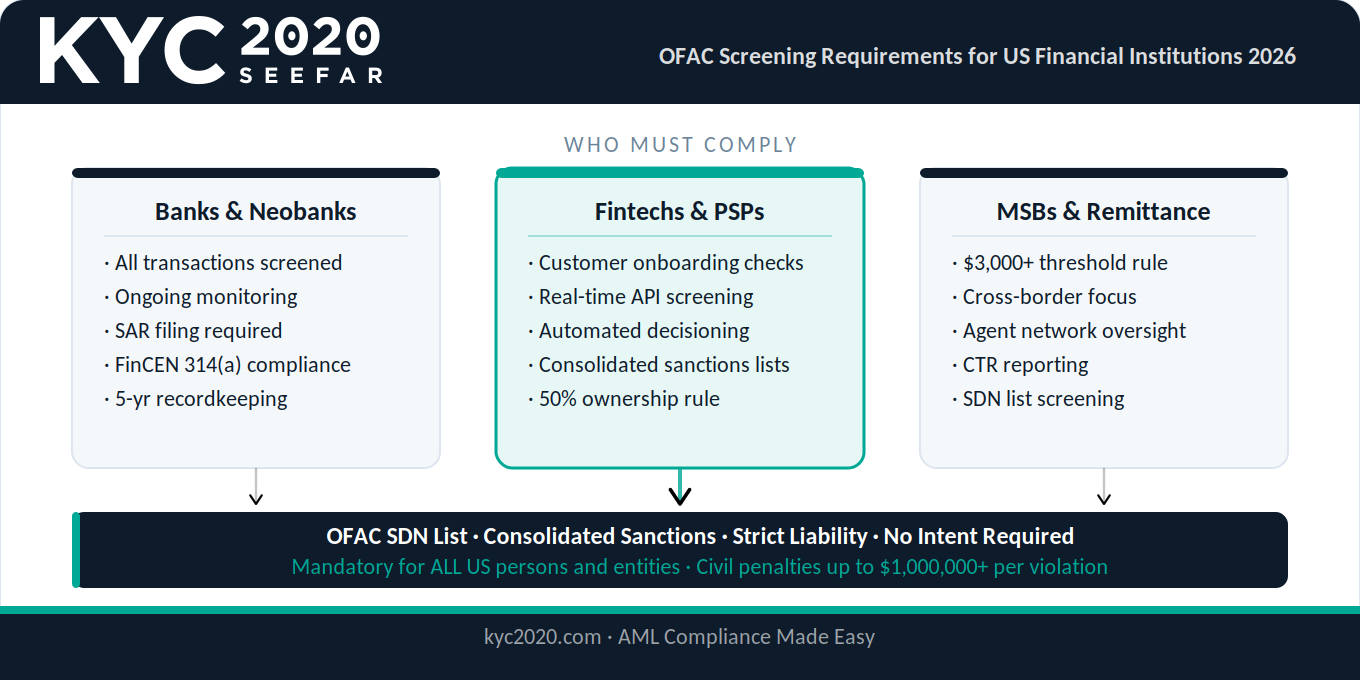

Large financial institutions, particularly large banks, aren’t strangers to the process of KYC and AML compliance. They are the largest influencers on the third-party AML compliance solution marketplace. The tools to tackle these issues have existed for a while now so why can’t SMEs just repurpose these systems for their own usage?

These tools are built for major financial institutions with whole departments dedicated to operating these programs. They need an abundance of staff and cash to run and it’s simply overkill for most SMEs. It’s like using a sledgehammer where a thumbtack would do. Ostensibly they do the same thing but the sledge hammer requires a lot more energy to operate and creates a huge margin of error. While large banks can afford the labor to use these systems, they simply aren’t feasible options for smaller companies. Moreover, the level of scrutiny most SMEs require isn’t on the same level as massive financial institutions.

Picking the Right Tool for the Job

Let’s put it this way. If you screen every sanctions list in existence, you’ve done everything possible to stay compliant with AML sanctions screening regulations. It’s more labor intensive but every imaginable base is covered. Major banks need this type of functionality. They risk massive repercussions if they make a mistake as wrong doers are constantly trying to take advantage of them. SMEs don’t have the same risk factors. They don’t need the same level of scrutiny as large financial institutions. This is where a ‘risk based’ approach comes in.

That is to say, a solution that matches the level of risk a SME takes on. Businesses conducting low risk transactions, don’t need to cover every base imaginable. Using strategic analysis, they choose to screen, not just the right number of lists but, instead, the lists that are mostly likely to yield results. This approach assures that level of labor required stays within the bounds of what is necessary for an SME to conduct their business responsibly.

AML Screening for the Next Generation

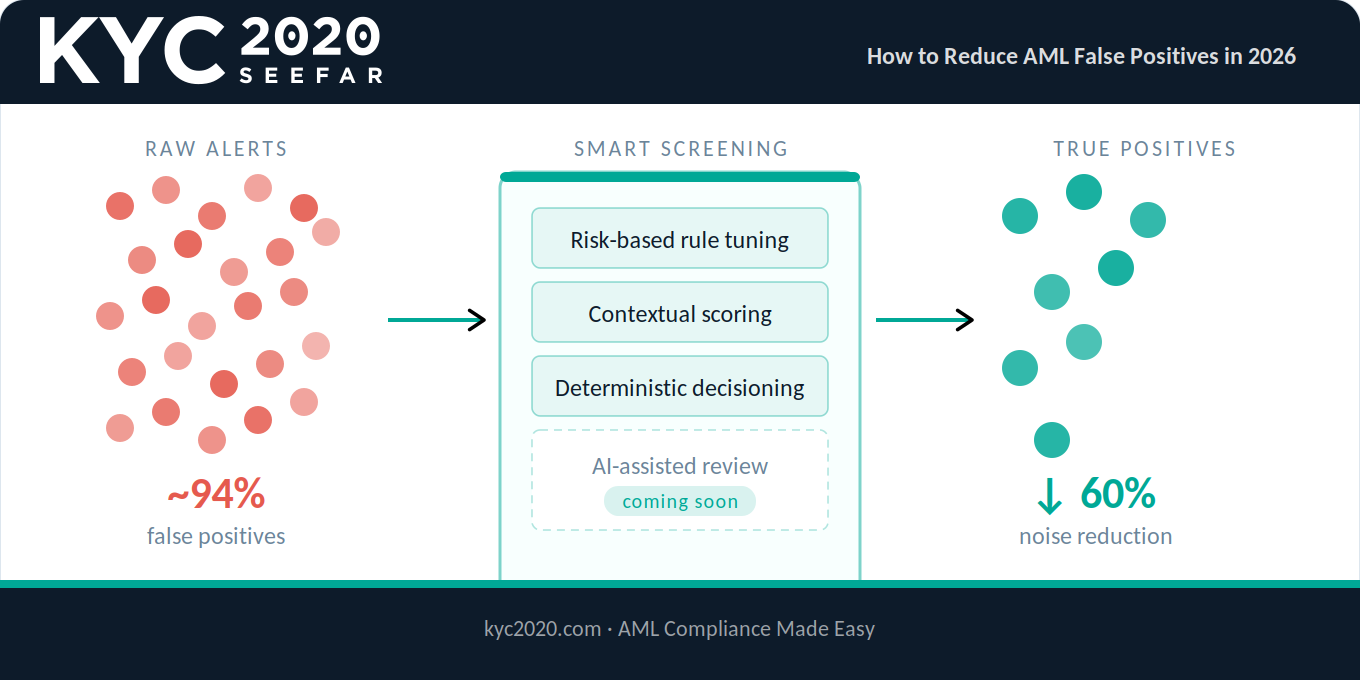

In order to keep up with the evolving markets and rising amounts of financial crime, SMEs need a new approach to sanctions screening. Decisioning systems are built with online businesses in mind. They are intelligent, self learning programs which can render 95% of all verification decisions automatically, within a 60-second time frame. They are easy to integrate into transaction workflow processes which are fast, effective, and self-perpetuating.

This approach lowers the frequency of false positives. Regardless, even the most highly tuned systems will have false positives to process and require a trained expert to handle. The fact of the matter is that human oversight is required in these processes but who has time for that when the marketplace is moving so quickly? Well, there’s a solution for that too. But we’ve talked a lot about problems at this point so let’s jump into the solution, DecisionIQ.

KYC2020 offers an easy, inexpensive way for SMEs to access and incorporate an appropriate level of screening for their purposes. DecisionIQ is a service built to be affordable, accurate, and transparent. If you want more information, check out our white paper.