What You Need to Know in 2026

The Office of Foreign Assets Control (OFAC) administers and enforces US economic and trade sanctions. Every US financial institution has legal obligations to screen customers, counterparties, and transactions against OFAC sanctions lists. Many non-financial businesses also must comply with these rules. Violations can result in civil penalties of up to $1 million per violation. Furthermore, criminal prosecution and reputational damage are difficult to recover from. This guide explains what OFAC screening requires, who must comply, what lists you need to screen against, and how to automate the process for a US institution of any size.

What Is OFAC and Why Does It Matter?

OFAC is a division of the US Treasury Department. It maintains a list of individuals, companies, and countries subject to US economic sanctions. This means US persons and entities are generally prohibited from doing business with them. The most important OFAC list is the Specially Designated Nationals and Blocked Persons (SDN) list. This list names individuals and entities whose assets are blocked and with whom US persons are generally prohibited from dealing. OFAC also maintains sector-specific sanctions programs targeting Iran, Russia, North Korea, Cuba, and Syria. In addition, there are programs targeting narcotics traffickers, weapons proliferators, and cybercriminals.

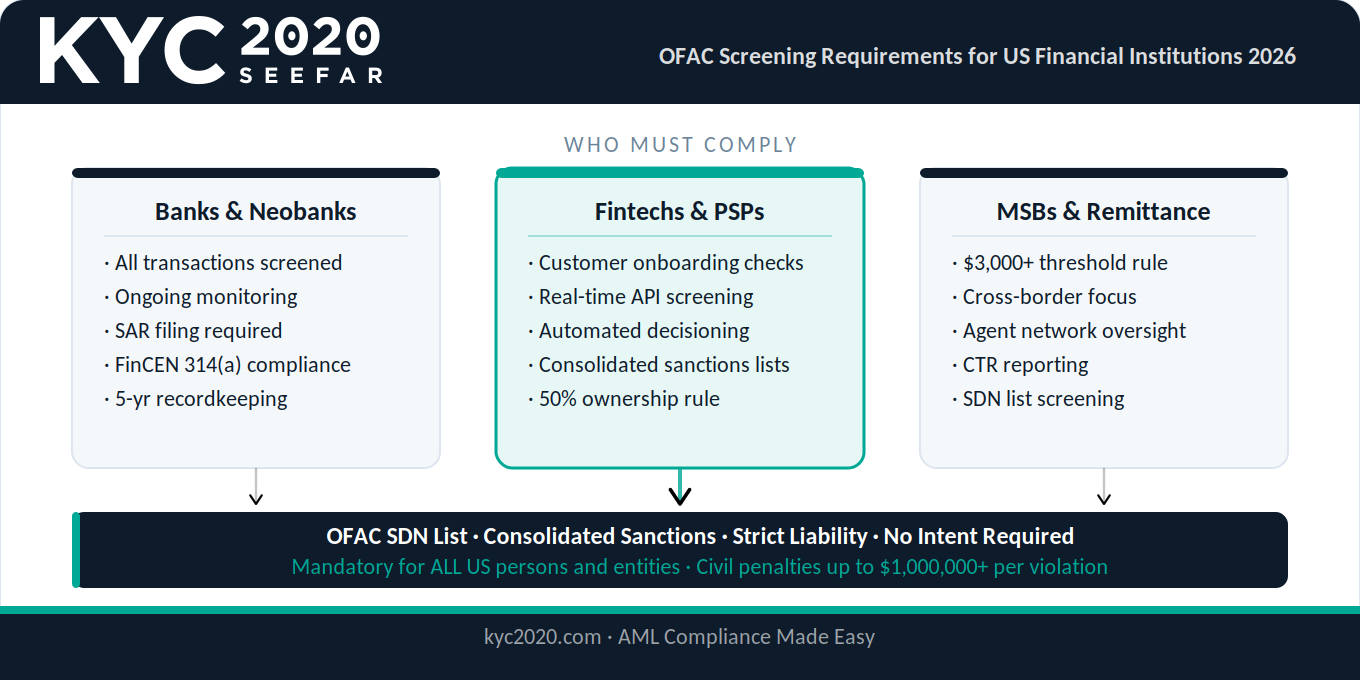

Who Is Required to Comply With OFAC Screening?

OFAC’s jurisdiction is broad. The following types of US entities have mandatory OFAC screening obligations:

- US banks, credit unions, and bank holding companies

- Broker-dealers and investment advisors

- Money services businesses (MSBs), including money transmitters, currency exchangers, and check cashers

- Insurance companies

- Fintech companies and payment processors with US nexus

- Import/export businesses dealing in goods subject to sanctions

- US persons engaging in transactions with sanctioned countries or individuals Foreign financial institutions that process US dollar transactions through US correspondent banks also have indirect OFAC exposure.

What Does OFAC Screening Actually Require?

OFAC does not prescribe a specific screening methodology. It requires that organizations maintain a sanctions compliance program appropriate for their size, risk profile, and complexity. At minimum, a functional OFAC screening program must:

1. Screen all customers, counterparties, and transactions against the SDN list and applicable sectoral sanctions lists before doing business

2. Screen on an ongoing basis – when sanctions lists are updated, existing customer databases should be re-screened

3. Block or reject any transactions involving a match, and report blocked assets to OFAC

4. Maintain records of all screening decisions for examination purposes

5. Train relevant employees on sanctions obligations and escalation procedures OFAC enforcement guidelines treat the strength of a compliance program as a mitigating factor in penalty calculations. Institutions with robust, documented screening programs consistently receive lower penalties. Moreover, they may receive no penalty at all for violations discovered voluntarily.

OFAC Screening and FinCEN: How They Work Together

OFAC screening is separate from – but closely related to – FinCEN’s Bank Secrecy Act (BSA) requirements. FinCEN requires covered financial institutions to implement Customer Identification Programs (CIP), conduct Customer Due Diligence (CDD), identify beneficial owners of legal entity customers, and file Suspicious Activity Reports (SARs). In practice, a complete US AML compliance program includes both OFAC screening (to prevent transactions with sanctioned parties) and BSA/FinCEN compliance (to prevent money laundering and terrorist financing). Most modern compliance platforms handle both in a single integrated workflow.

How to Automate OFAC Screening for a US Financial Institution

Manual OFAC screening is impractical for any institution processing more than a handful of transactions per day. Automated OFAC screening software handles the process in real time, at scale, with full documentation. A modern OFAC screening platform should:

- Screen against the OFAC SDN list and all applicable sectoral sanctions lists in real time

- Update automatically when OFAC publishes list changes (OFAC updates its lists without advance notice)

- Apply name relevancy scoring to catch name variations and transliterations

- Generate an audit record for every screening decision – both matches and non-matches

- Integrate with your onboarding workflow via API, so new customers are screened before accounts are opened

- Support batch screening for periodic re-screening of existing customer portfolios KYC2020 provides all of these capabilities, covering the OFAC SDN list, OFAC consolidated sanctions, and 1,500+ additional global watchlists – in a single platform that also handles FinCEN CDD, BSA identity verification, and ongoing monitoring.

KYC2020 is an AML compliance platform built for US financial institutions. Our OFAC screening covers the SDN list and all OFAC sectoral sanctions. It also covers 1,500+ global watchlists with real-time updates, automatic audit documentation, and API integration that deploys in under 5 hours. Trusted by US and Canadian compliance teams for over 10 years.